The Productive State

On Governing The Supply Side

This month at Forces of Production, to celebrate the 250th anniversary of America’s Declaration of Independence, we are declaring an approach to policy: the Productive State. Today’s special newsletter is the first of our semi-regular policy briefing series, introducing the Productive State policy framework for governing the supply side, which will guide our future analysis at Forces of Production.

The Productive State

Looking ahead to the next political cycle, a consensus left agenda is clearly forming around two sets of goals. One set for the American economy – stability, growth, innovation – and another for the American people: affordability, equality, better work, and a sense of shared control over our economic future.

Each of these consensus goals points to a pervasive dissatisfaction with the supply side of the economy, where private capital determines what goods and services are produced, who can afford them, and even what kinds of jobs exist. Today, that supply side is organized mainly to produce profits, with no view to the unaffordability, stagnation, inequality, and volatility that the single-minded pursuit of profit creates for all.

To produce a better life for all, policymakers will need to govern the supply side. Doing so will require tools more powerful than the tax breaks, tighter regulations, and targeted subsidies that policymakers have so far relied on. It will require a real restructuring of the supply side based on a better map of our economy — a map of its real productive capabilities and its global dependencies. Any plan for achieving the next progressive economic agenda must be able to answer two questions:

How is the economy we want to build structured?

What policy tools will be needed to build that structure?

At Forces of Production, our mission since first setting off has been to chart the waves of the supply-side economy while tracking the currents beneath. Today, our goal is to show a route across the economic seas to a more democratic, dynamic, and decarbonized economy. Today, we share the first design plans for a policy vessel we think is capable of making the journey: the Productive State.

The Productive State approach brings the state to the supply side, where it can govern the economy using the economic powers of public ownership to directly plan, coordinate, invest, produce, and provide.

For decades, corporations have used these same tools privately to build an economy that only guarantees profits can be extracted instead of guaranteeing the public interest is served. The Productive State uses them to restructure key sectors and supply chains towards our shared goals in ways that taxes, transfers, and tinkering at the margins of the private market simply cannot.

The Productive State shapes the supply side by redesigning key sectors and structures of the macro economy around our collective goals. By participating directly in the supply side as a core actor, the Productive State can publicly provide the essential goods and services of a dignified life, most importantly energy and healthcare.

The Supply Side and the Productive State

Since the New Deal, American political economy has operated on a division of labor between the state and market which has given the private market control of the supply side and made the state responsible for the demand side. That demand-side responsibility is critical — fiscal spending to fight recessions, welfare to sustain households, and unemployment insurance to support jobhunters — but limited. Once private capital and market exchange have produced real world outcomes on the supply side, the state taxes a share and redistributes it in various forms. While this demand-side smoothing is a lifeline for many, it cannot change how those sectors are organized, who profits from them, or what their products cost.

The supply side is where most important long-term decisions about the economy are made.

By “supply side”, we mean the structure of production itself: the local and global network of equipment, workers, and organizations that coordinate to produce the goods and services purchased by consumers on the demand side. These are shaped by patterns of investment and divestment in productive capacity and infrastructure. This network is disaggregated into sectors, industries, and institutions that all shape the structure and capabilities of the entire economy through the unique roles they each play, and the unique technical dynamics at play in each sector.

The supply side is a mammoth apparatus. It encompasses the grid that powers homes and businesses, the healthcare system that treats patients and employs a tremendous amount of the US workforce, the housing stock that people live in, the manufacturing base that produces essential goods, and every point that coordinates trade with the global economy. Across all this activity, private capital remain the primary decisionmakers, which in turn has meant that investment, production, and provision remain fundamentally organized around the goal of private profit.

The demand side is where decisions about the present, rather than the future, are made.

What to have for dinner, which kind of car to buy, whether to go on vacation — these demand-side decisions connect the supply side to household consumption. On the micro level, the state is responsible for ensuring that everyone has sufficient purchasing power to demand the basics of a dignified life. On the macro level, the state is tasked with managing the demand side of the private market through fiscal and monetary policy to prevent recession and keep the private economy growing even when investors grow worried, by supporting rising consumption.

The state can and should use demand-side tools to govern the economy towards full employment and high investment. However, this division of labor between the state and the private market leaves the governance of the supply side entirely up to private capital and market dynamics. This leaves the answer to almost every important economic question up to profit-seeking private actors — what gets built, what services are provided, by whom, at what cost, over what time horizon, and to what end. Which sectors of the economy get organized in which way determines everything: prices, investment levels, who benefits, where and how people work, whether decarbonization happens at all. The supply side is currently predominantly structured by the interests, logics, and capacities of private actors, which means that when private capital fails to build, produce, or provide in the ways society needs, there is no one to hold responsible.

A state with only demand-side tools can subsidize the purchase of housing, healthcare, and childcare, but it has no power over their supply. Answers to questions of pace, scale, quality, labor conditions, and the price of essential goods and services remain dictated by private capital.

The perspective of private capital is necessarily limited to profit and increasing financialization has further narrowed its vision. Immaterial investments into patents, copyrights, and software — including so-called “Capital-Light” strategies like those pursued by NVIDIA, among others — have prioritized the development of global capacity rather than local, while domiciling profits across a range of tax havens. Private investment at the cutting-edge of healthcare and pharmaceuticals has led to rising profits and a collapse in standards of care across less-wealthy areas. With automakers needing to profit on their Electric Vehicle lines, they have chosen to shut them down and roll back investments as the Trump administration eliminates the tax breaks that made those investments profitable. At the same time, workers and communities are forced to accept Silicon Valley’s preferred adoption strategies for AI usage and the siting of data center infrastructure, because those strategies are seen as the path to highest profits in a global competition of bank accounts.

When and How the Productive State Intervenes

The Productive State intervenes where markets and private capital have demonstrably failed. That means sectors where productivity gains have been exhausted and profit has become rent extraction rather than reward for innovation, where price increases cascade through the entire economy and threaten macroeconomic stability, and where private capital has created inflationary pressures through chronic underinvestment. In sectors that meet these criteria — especially those in which social need is unconditional, or the country has policy goals which the private supply side is not organized to deliver — the Productive State brings public power directly to the supply side.

The Productive State intervenes by deploying the economic powers of public ownership to reshape these targeted sectors. In some cases, this means the use of strategic reserves to stabilize volatile prices — extending the logic of the Strategic Petroleum Reserve to encompass generic drugs, critical minerals, and commodity semiconductors alongside other raw materials and intermediate goods. Where a stronger intervention is required, the Productive State charters public corporations to serve as anchor producers capable of changing the terms on which private markets operate or displacing private capital entirely. With these tools, the most essential goods and services — healthcare above all — can be decommodified and universally provided free at point of service as public K-12 education is today.

Bidenomics got two important things right: the supply side matters and public spending should be directed toward productive ends. Between the semiconductor investments of the CHIPS Act, the climate investments of the Inflation Reduction Act, and the large-scale fiscal spending of the pandemic recession response, Biden-era economic policy put critical pieces on the board but didn’t always wire them together correctly. Where the “derisking” approach tried to reshape the supply side by guaranteeing profitability to private investors, the Productive State embraces the full economic powers of public ownership — directing fiscal spending to build and own productive capacity directly instead of solely relying on subsidizing private investment.

The Economy of the Productive State

Market organization can lead to great decisions that advance the economy’s growth and innovation frontier. But those same market processes are often terrible at stability and maintenance — at making sure no one gets left behind in the process. The results of leaving the supply side entirely to private capital are clear in our increasingly unaffordable essentials, chronic underinvestment in productive capacity and infrastructure, K-shaped labor market, and weak productivity growth (outside of a narrow band of highly profitable sectors).

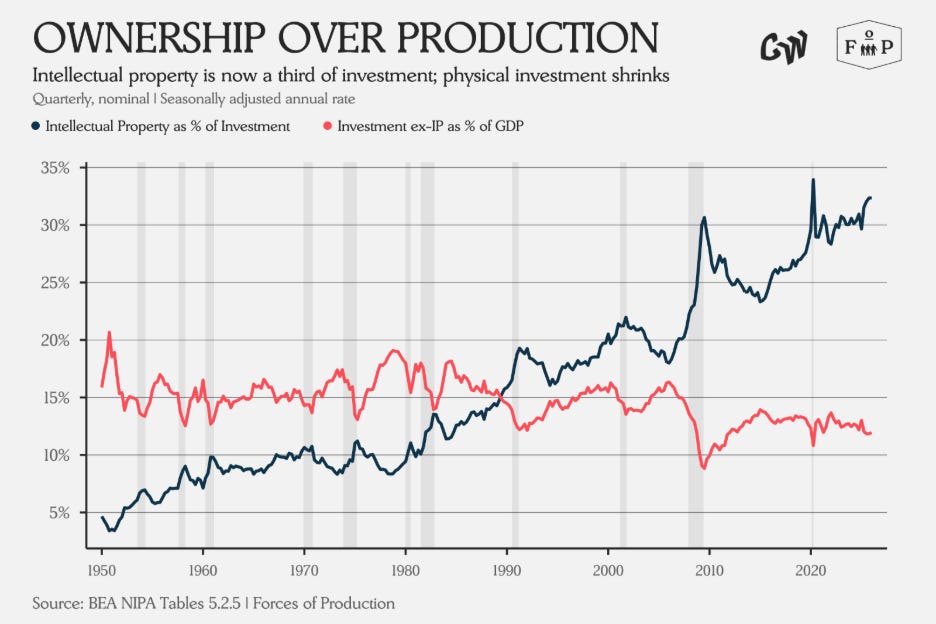

The single-minded focus on profits has also dematerialized investment. As profits have concentrated in the ownership of immaterial assets — patents, copyrights, software — investment in the material side of the economy has steadily fallen as a share of GDP. Although more dollars are being spent every year, a smaller share of those dollars go to real steel-in-the-ground physical investment than ever before, while intellectual property products now account for a third of the value of all private investment each year.

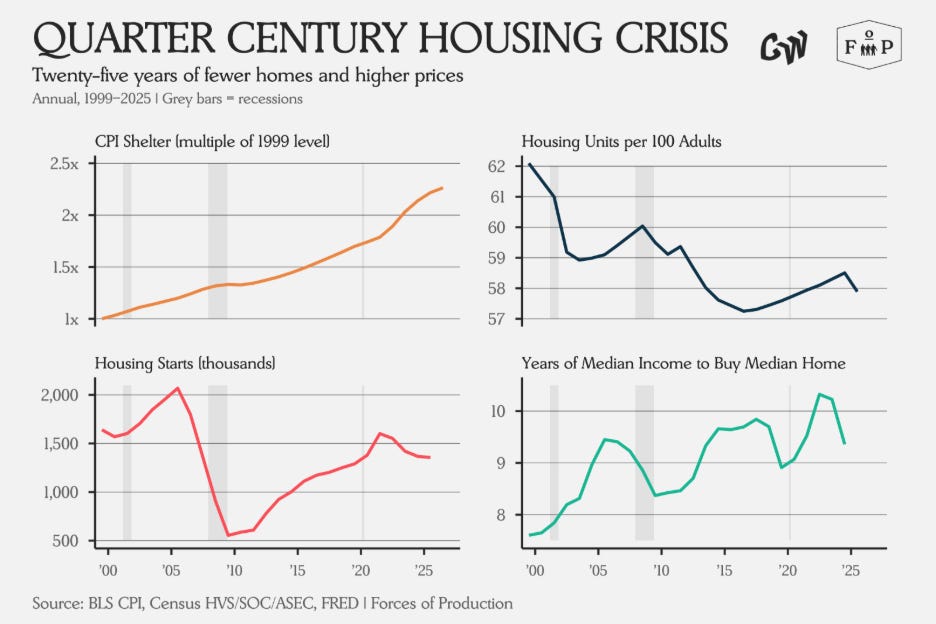

As a result, the basics of a dignified life have grown more expensive as private actors decline to expand capacity in ways that might risk their profitability. In housing, we see this through a crisis of underbuilding brought on by the collapse in the financial value of housing during the Great Recession. When it became unprofitable to build, homebuilders stopped building and went out of business or consolidated. The government, lacking supply-side tools of its own, did not step in. The result is the crisis of rising prices, swelling backlogs, and soaring rents we see today.

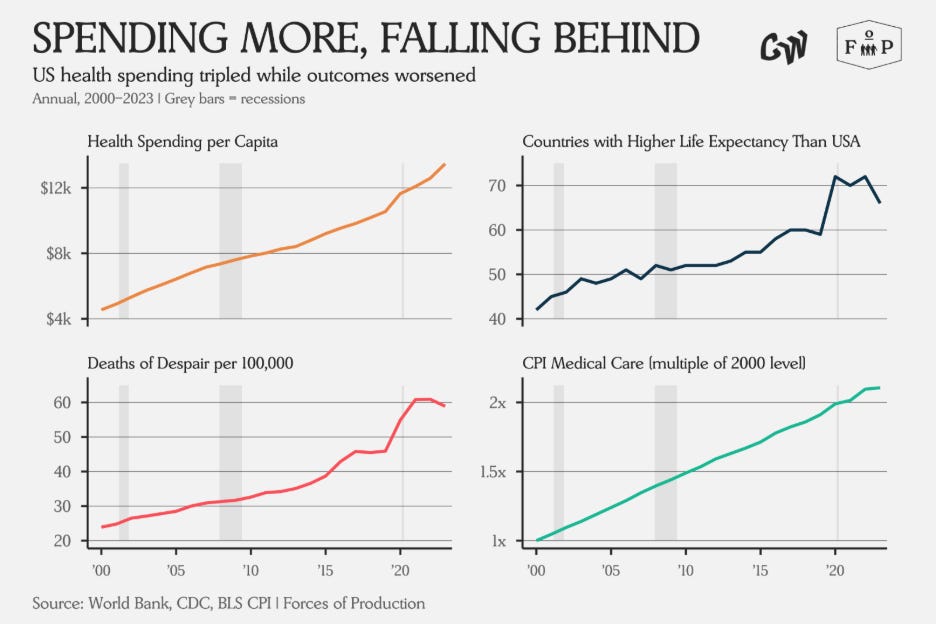

Healthcare prices and spending have continued to rise even as the US falls in the rankings for health outcomes, spending significantly more per capita than peer countries for shorter lives and worse care. The healthcare sector absorbs a growing share of GDP while the cost burden increasingly falls on households — a structural failure better addressed through the supply side than public subsidy of healthcare consumption or income transfers.

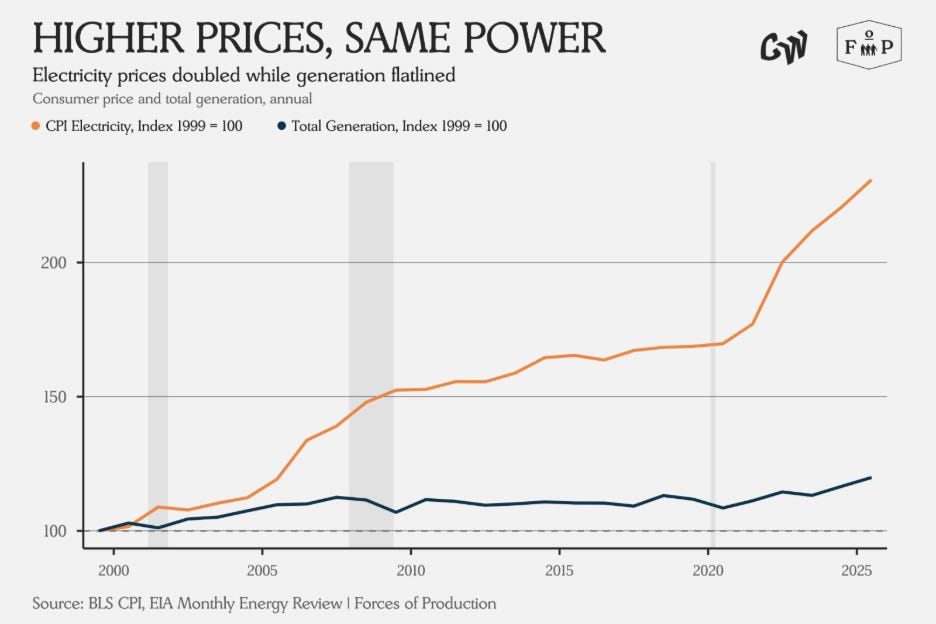

Electricity prices, too, have risen faster than electricity output, as a fragmented and profit-driven grid struggles to support the energy transition or absorb new demand from electrification and data centers.

Solving these problems will require a Productive State capable of intervening on the supply side, taking over the tasks that private capital has shown it is not interested in doing well. By investing in and publicly providing essential goods and services at cost, the state can give society democratic control over key macro-structural economic decisions which would otherwise be made for private capital, by private capital. This means decommodifying essential goods and services, building the infrastructure that private capital has declined to build, and stabilizing systemically important prices through public ownership at critical chokepoints.

Public investment, production, and provision at this scale would transform the economy and society alike by building out a new foundation to make them work for everyone. The result would be a high employment economy with affordable essentials, stable prices, cheap clean energy and a genuine say over the economic forces that structure everyday life. With the Productive State approach, Americans will have more freedom to take the kinds of risks — starting businesses, changing careers, striking out into the wilderness — that our culture celebrates but which today’s economy makes impossible for most.

From The Economy We Have to the Economy We Want

Where do we start building the Productive State to take us from the economy we have to the economy we want?

We propose an interlocking policy architecture linking a Public investment Authority, Public Health Care, and a Federal Grid authority as the institutional and economic foundation for a high-investment, low-emission economy shaped towards democratic and productive ends.

The Public Investment Authority gives the Federal government access to the powers and tools of large-scale public ownership to plan, coordinate, invest, produce, and provide. A Federal Grid Authority would be empowered to standardize, rationalize, and decarbonize the energy system towards a goal of decommodifying basic access to energy. A publicly owned health care system where services are provided free at point of service would remove the most volatile share of household budgeting from affordability conversations entirely and curb one of the fastest-rising costs for businesses.

While we do not have space to outline the specifics of these programs here, our goal is to demonstrate that this interlocking policy architecture will build a foundation in the Public Investment Authority, then the infrastructure of the Federal Grid Authority before delivering on health care and energy for all Americans.

Public Investment Authority

To durably intervene and restructure the supply side, the Federal Government needs a central authority for orchestrating, coordinating and funding the large-scale investment that will be necessary in the economy of the 2030s. This should take the form of a Public Investment Authority capable of coordinating with firms, capital markets, bond markets, and government agencies to provide a linchpin for macroprudential supply-side governance.

Rather than derisking or subsidizing the private market, the Public Investment Authority puts long-term public capital into projects that stabilize and standardize the supply side, from grid equipment and next-generation steel and minerals to rural hospitals and urban childcare centers. Changing the structure of the economy, and not just the current equilibrium, means changing what gets built, by whom, and who owns it.

Federal Grid Authority

The electrical system plays a role in every household and process of production in the US economy. China organizes its electrical system around supporting both, while we have chosen — except in some existing pockets of public ownership — to organize the American system around extracting profits from both. This raises costs for households and firms alike, squeezing family budgets and making American goods and services more expensive on the global market.

The drive for profitability has also set up complex and sclerotic fiefdoms incapable of adapting to a decarbonizing world or supporting the load growth required to electrify major industries. The addition of a few data centers should not be an energy affordability crisis for everyday Americans, but our private grid system has made it one.

A Federal Grid Authority would intervene as a supply-side coordinator, bringing the whole network into public ownership so that it can be standardized, decarbonized, and retooled in support of our electric future. At the same time, the Federal Grid Authority can serve as a nexus point for affordability through decommodification. A social minimum of energy, like the standard deduction on federal income tax, would directly free up space in stressed household budgets. At the same time, the Public Investment Authority can continually invest in new clean generation to increase that social minimum, and eventually provide free energy to households, public schools, and even private firms.

Public Health Care

Rising demand for services, in particular health care, will be a major dynamic of the economy of the 2030s. Health care absorbs nearly a fifth of total US spending every year, and as demographics shift, demand will continue to rise, leading to expensive and rationed care without a significant supply-side buildout. As it stands, peer countries deliver better outcomes using a dramatically smaller share of GDP.

Public Health Care means decommodification and public provision — health care free at point of service, run and funded by the public sector. Instead of directing spending to the massive administrative overhead required to deny care through the insurance system, that same money can be used to expand capacity, access, and quality of care, which is also an issue of labor conditions. As with the Federal Grid Authority, the first step is to take existing assets into public ownership and then rationalize, reconstruct, and rebuild around the task of delivering the best care at the lowest cost with the fewest middlemen between. As it stands, the sector is consolidating and centralizing on the supply side, but consolidation through public ownership captures those benefits without corporate profiteering or bloat.

This will have to be done in stages, and second-order effects will need to be managed, including a massive ramp-up of public investment into pharmaceutical and medical R&D as well as a national federal hiring campaign to utilize the talents of displaced insurance and administrative workers.

Bringing the state to the supply side through these three policies would revolutionize affordability for everyday Americans while providing a competitive boost to US firms on the global market. Publicly provided health care and energy would remove two of the largest and most volatile line items from household budgets while doing the same for businesses across the country. Removing these sources of uncertainty would empower workers to start their own productivity-enhancing firms while helping level the playing field between small and large businesses. These are the ingredients of an economic boom built on a foundation of pragmatism, equity, and shared abundance.

The Journey Ahead

The full Productive State will take time to build and will require a complex mixture of institutions and tools capable of adapting to a changing supply side. Right now, the Trump administration, the tech billionaires, and endless petty scammers and frauds of all kinds are looting our economy and warping our society around their noxious goals. The response must be to take up the real task of economic reconstruction to reshape the supply side around public need instead of private profit.

At Forces of Production, we will be working to put all the pieces of the Productive State approach on the board, and pursuing the research we believe will be necessary to guide our economy from its extractive present to its democratized and decarbonized future. Taking up the task of actually governing the supply side raises hard and open questions about the kind of economy we are building for ourselves and our children, how to provide stability, growth, and a real economic voice to all people.

As we are assembling a body of research organized around those hard and open questions, future issues will explore a range of topics around and beyond the following:

Affordability

What is the difference between “inflation” and the “cost of living” and how are each measured, and how do both concepts shape “affordability” or “real wages” in different ways?

How does the structure of production confer the power to propagate inflation on some sectors and not others, and how does that propagation shape the path of investment and capability development on the supply side and inflation on the consumer side?

How should programs like CalRX be expanded to deliver affordability through decommodification of essential goods and services?

Public Ownership

What kinds of dynamics will a shift from private accumulation towards public accumulation create for private markets and the global financial system?

Which institutional pinch-points are liable to slow, alter, or prevent the rollout of Productive State interventions?

Which sectors are the future of industrial policy, and what are the institutions required to coordinate them towards the public interest?

How can public investment be structured to “crowd in” the maximum amount of additional private investment?

How do we track and value public assets and the decommodified provision of goods and services? How does the value of public assets relate to the public balance sheet, the federal debt, and the obligations of the Treasury?

Growth and Investment

What is the future of productivity growth through automation and sectoral composition, and how can we credibly measure it? Which industrial policy interventions are meant to deliver particular outcomes, which to provide jobs for workers, and which are meant to shape the basic productive capabilities of our economy?

What are the growth trajectories for an economy organized around services, and how can we prevent the creation of a two-track K-shaped labor market that prevents people from realizing their full potential and making their full contribution?

How will the path of AI development drive the business cycle going forward, and how do implementations of AI tools in the workforce relate to the class struggle?

Economic Structure

What kinds of occupational roles are distributed across the economy, and how do they shape and constrain the ways we can build the economy of the future?

What will need to be done to deliver a fully decarbonized economy, and how will that change the structure of production, affordability and global competitiveness?

What must be done in upstream supply chains for decarbonization of electricity and electrification of the economy? How will institutions and hardware cope with load growth that far exceeds data center load growth in the transition from a petrostate to an electrostate?

Which sectors are systemically important, where are the bottlenecks, and what could a supply-side vision of progressive globalism look like in terms of institutions and the global division of labor?

All of these questions, frankly, are just longform ways of asking how we can all work together to lend a hand against the choppy seas ahead.

If that simple, basic question interests you, then welcome aboard.

This Month’s Data

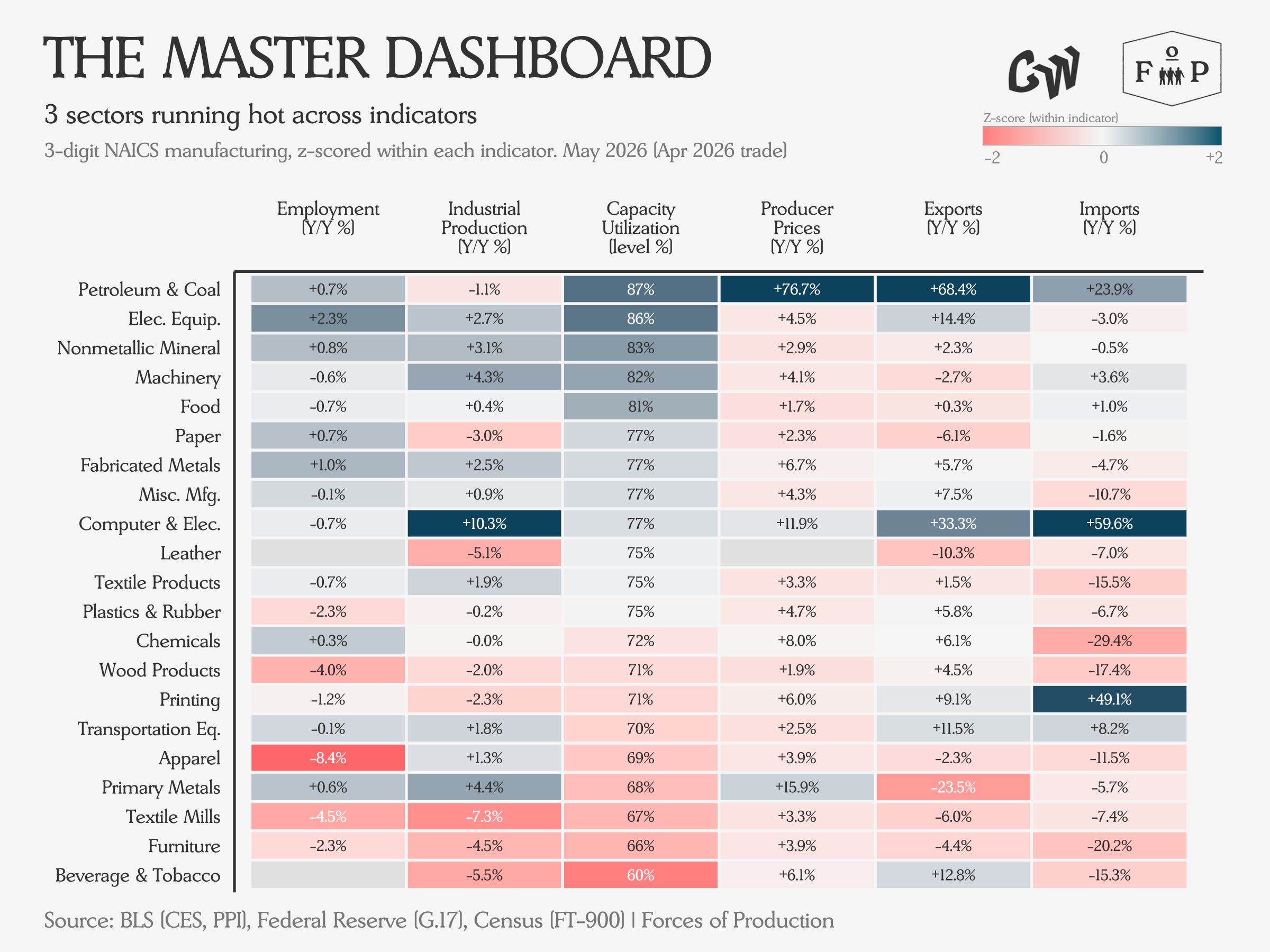

Here, we are looking at the May data, released over the course of June, with the exception of trade, which is released on a two-month lag, so there we are looking at data from April. Overall, we see the peak of the Hormuz shock (so far) in the PPI data for May and continue to see strong performance from Computers & Electronic Equipment, Electrical Equipment and the broader fossil fuel complex. To the extent that there is a single thematic, it is that the economy is building the Graphics Processing Unit and Power Supply for the nationwide meta-computer, and the terrain of struggle is over what kinds of sources will be fed into that power supply, and what it means for regular grid customers.

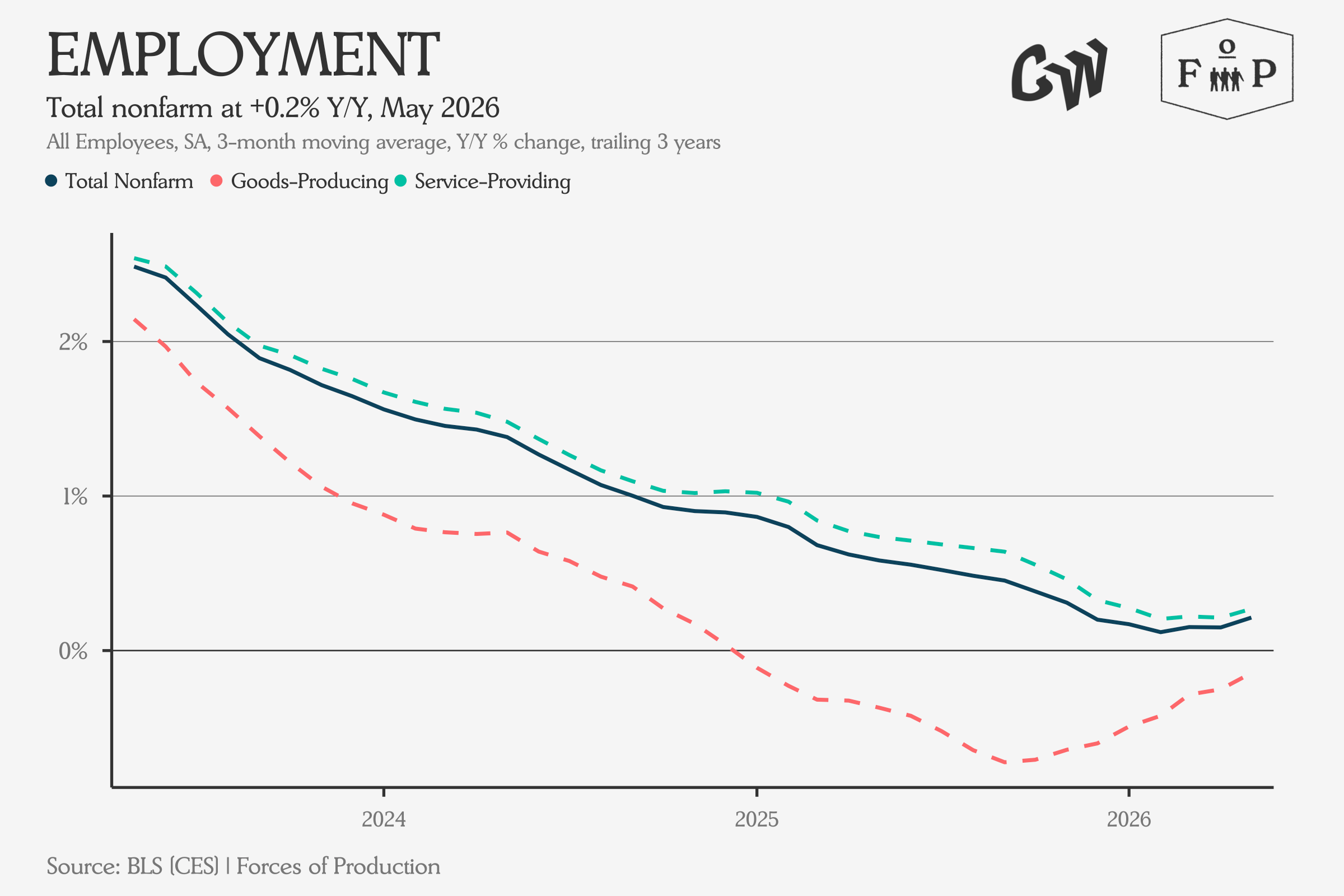

Everything outside of this thematic is a bit adrift, with prices broadly rising on the oil shock, capacity utilization holding steady, and industrial production inflecting upwards as the above thematic passes through different levels of the relevant supply chains. Even after revisions, employment additions came in strong even as, on balance, workers continue to slowly exit the labor force, holding down the unemployment rate.

Employment

May payrolls rose more than expected in the initial release, by 172,000, but after the first revisions to the May data released last week, measured employment actually only increased by 129,000. Despite this, financial markets broadly interpreted the ongoing rise in inflation alongside a growing labor market to indicate more interest rate hikes from the Fed in the back half of the year.

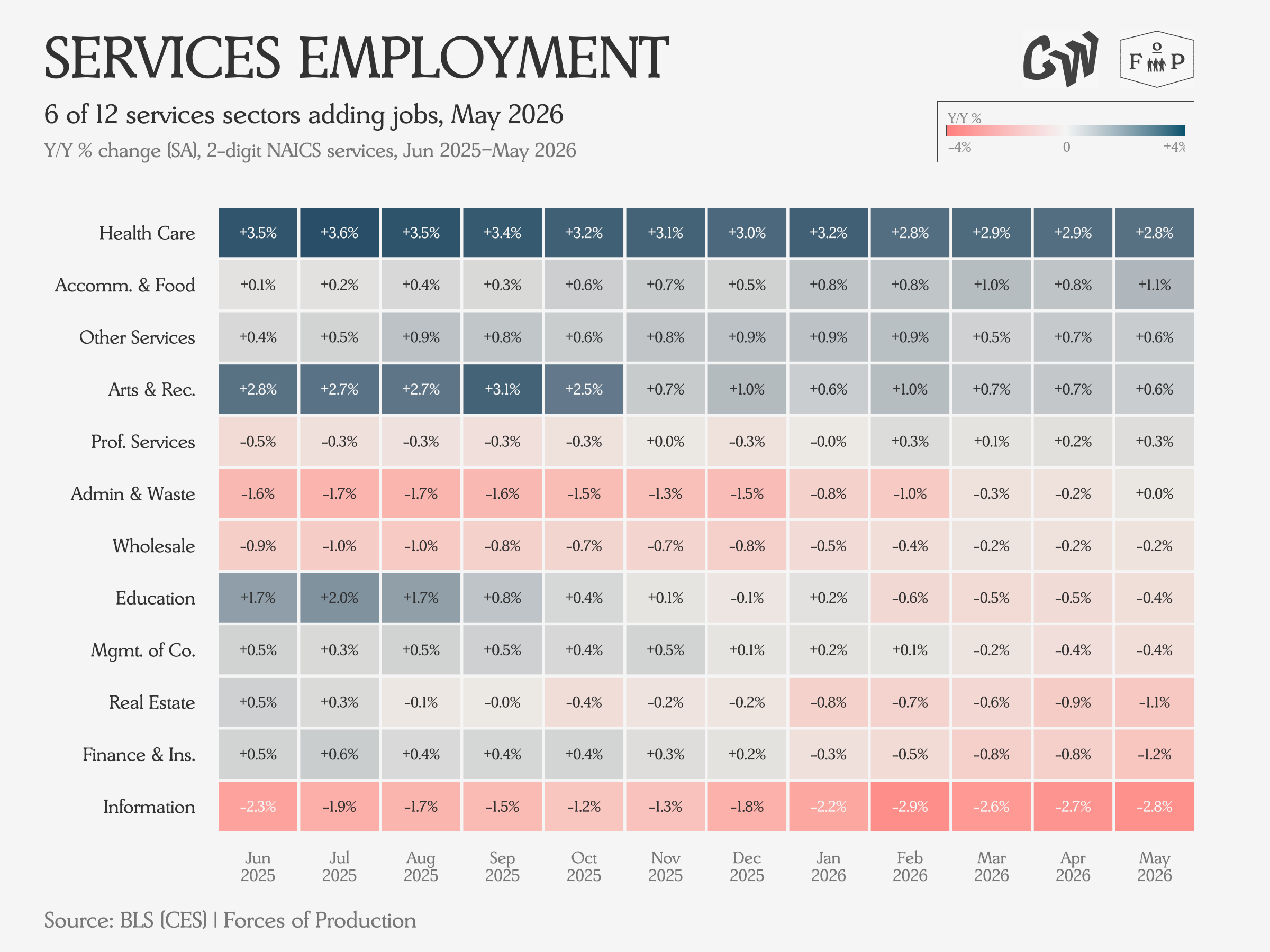

Looking at just the Service sector, Health Care continues to lead growth. Interestingly, despite the steady increase in production and imports for Computer Equipment, employment in Information Services continues to fall against the previous year.

Real Estate and Finance & Insurance are also beginning to see some acceleration in employment decline, with both going from +0.5% growth a year ago, to a 1.1% and 1.2% contraction, respectively, in the May data.

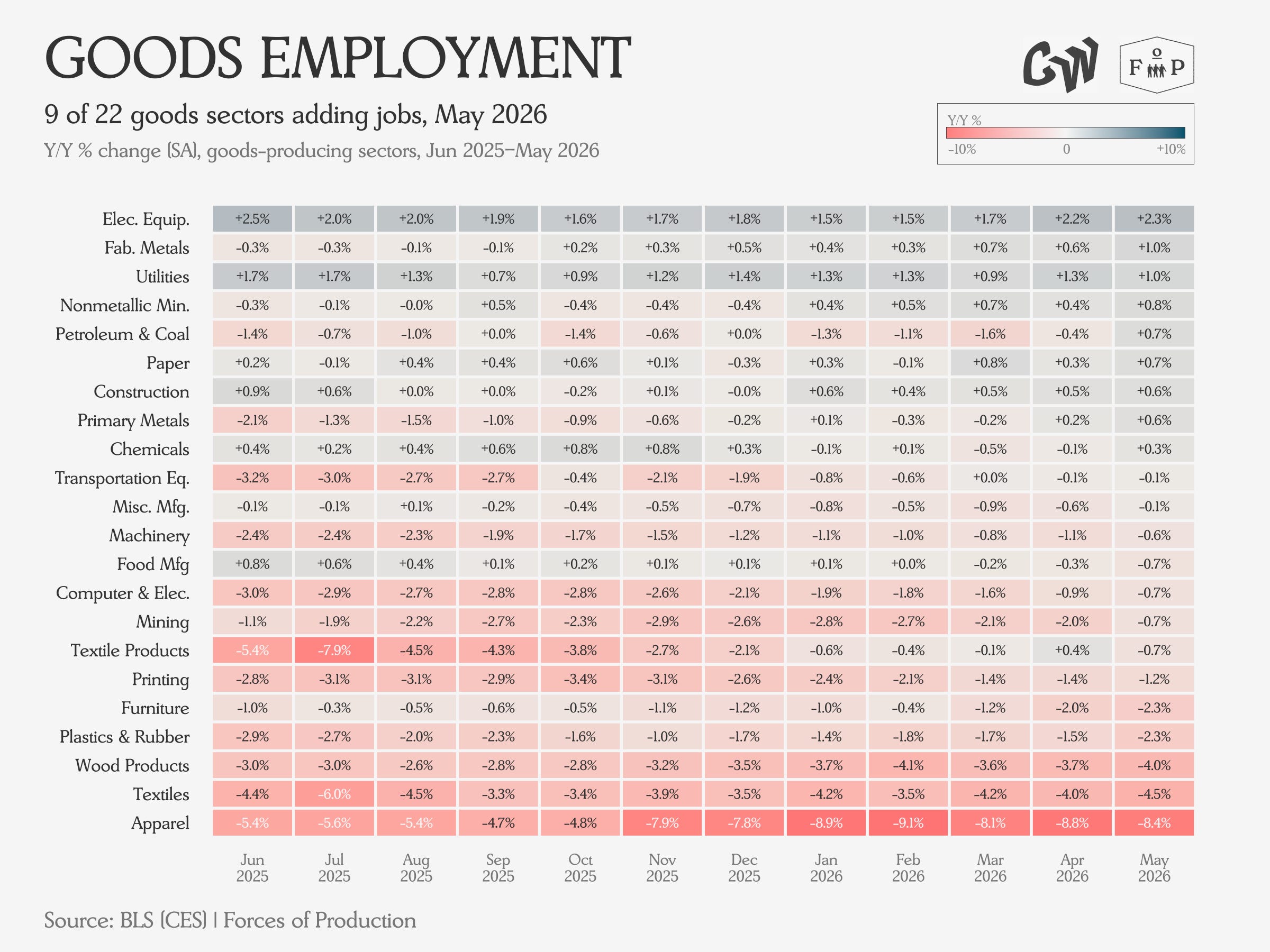

On the Goods side, we see employment in Construction beginning to mount a comeback, with Utilities and Electrical Equipment still consistently adding the most employees. Textiles and Apparel continue to be in acute distress, losing nearly 5% and 10% of total employees, respectively, over the past year.

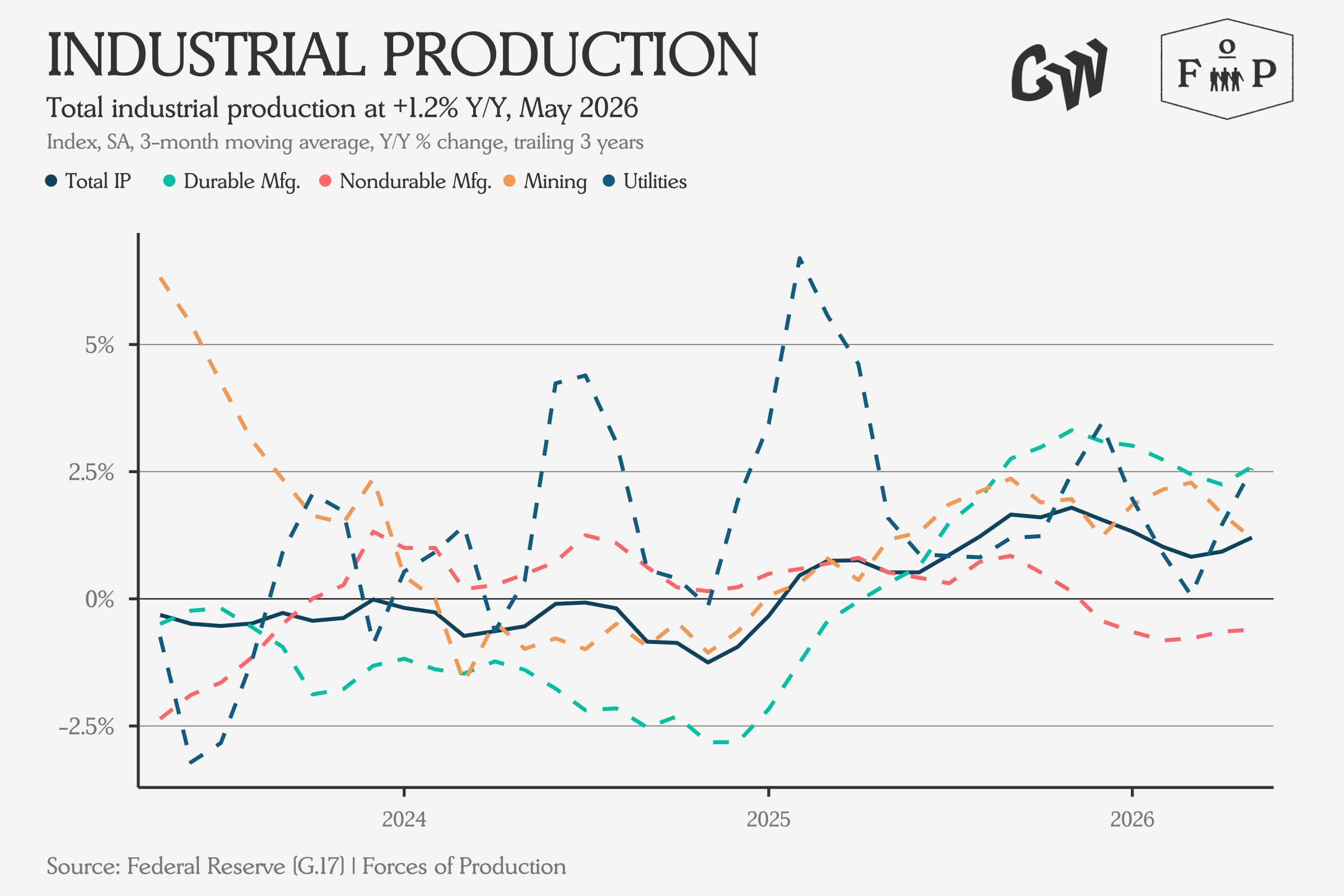

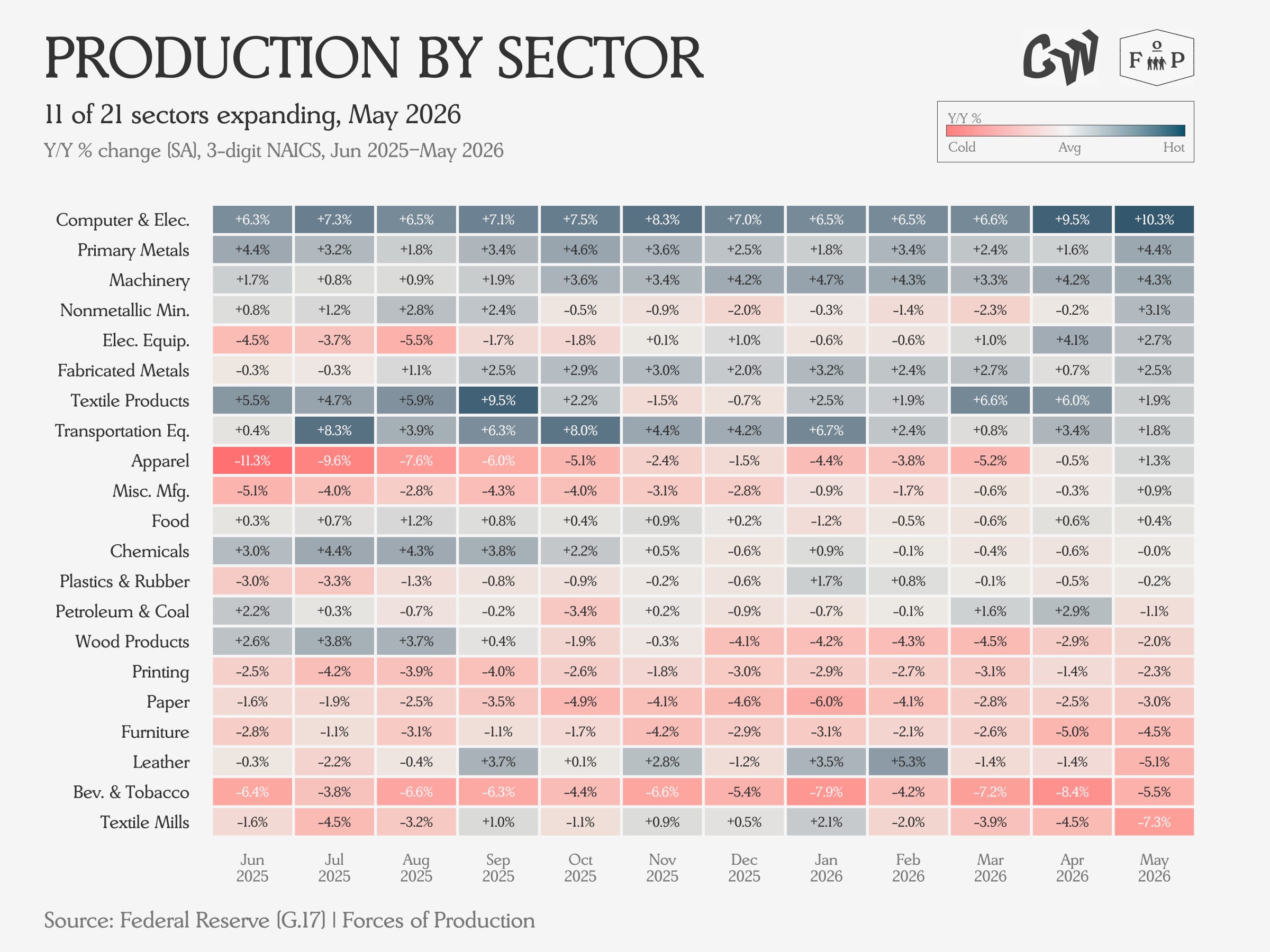

Industrial Production and Capacity

Durable Manufacturing and Utilities continue to inflect upwards in the May Industrial Production data, while Mining decelerates and Nondurable Manufacturing continues to contract. We see little movement from month to month which remains an improvement compared to the month after “Liberation Day”.

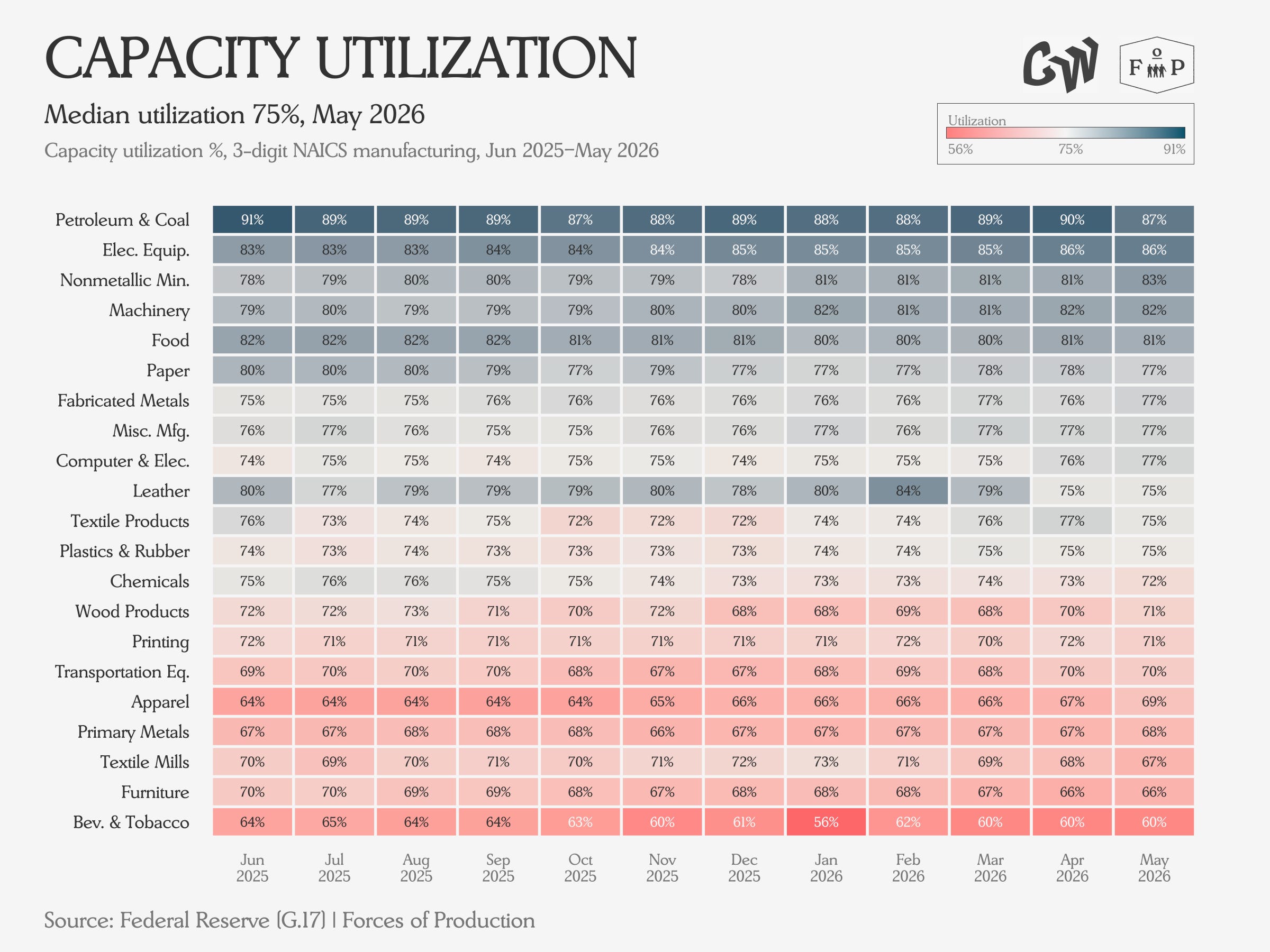

On the capacity utilization front, things continue to hold steady, with refineries ramping down a touch on the Hormuz crisis and Nonmetallic Minerals ramping almost 5 percentage points over the past six months.

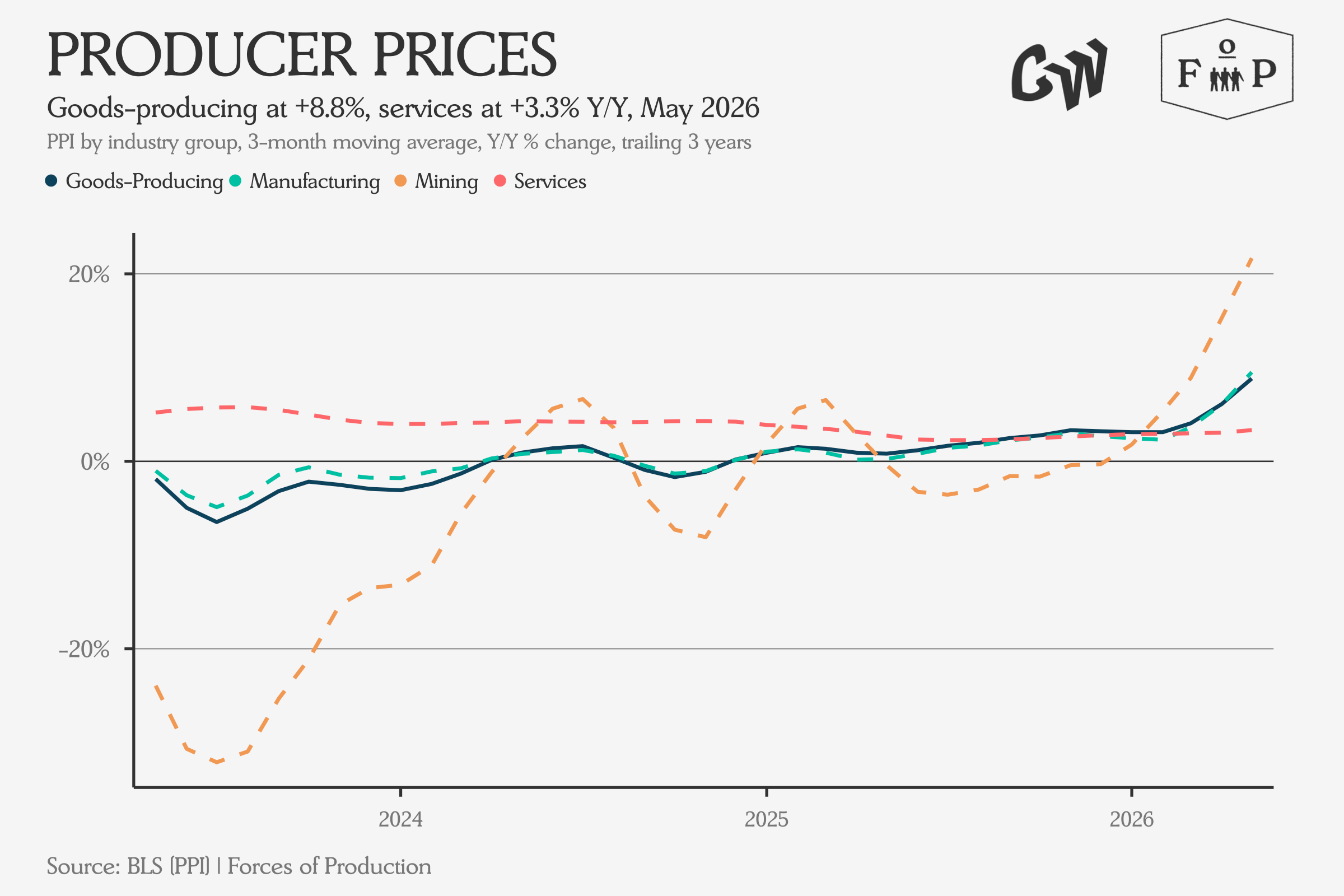

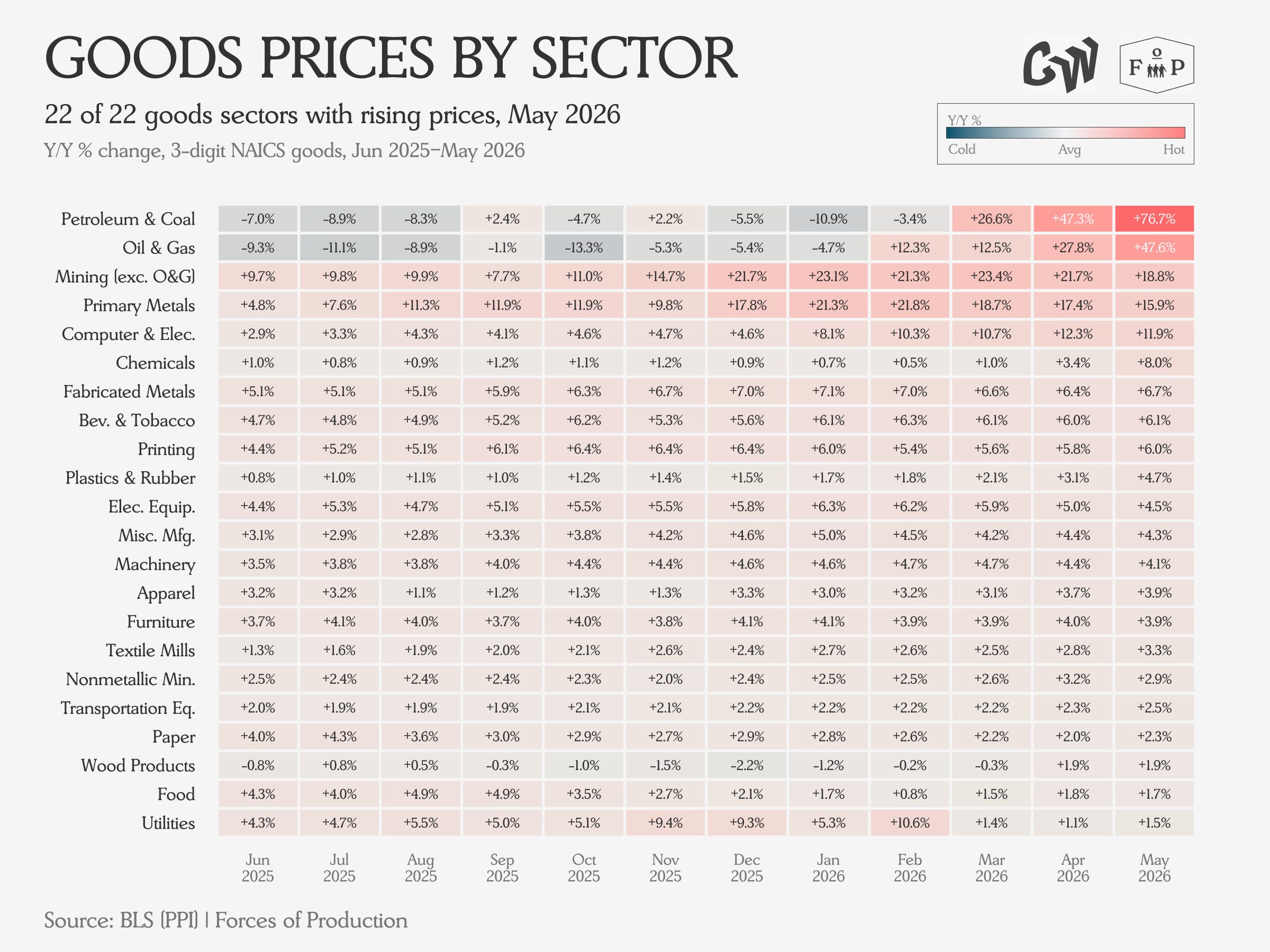

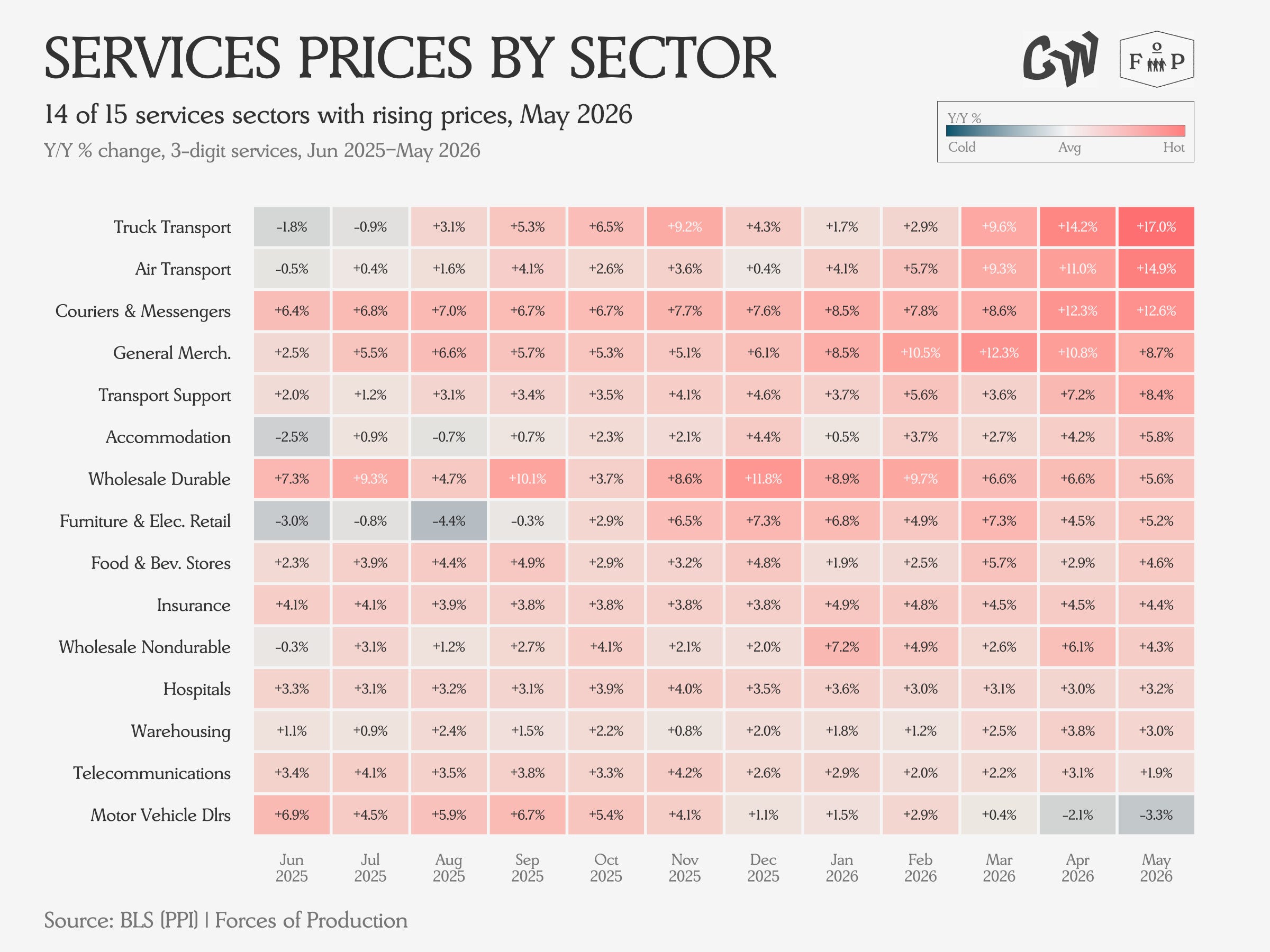

Prices

Producer Prices jumped dramatically in the May data on the strength of the Hormuz oil shock. We are beginning to see those prices pass through to other industries dependent on petroleum distillates in the May data, with goods production hit harder than services.

Looking across Goods-Producing sectors, we see some extreme price pressures due to Hormuz, but also long-simmering price pressures in Primary Metals, Mining ex-Oil & Gas, and Computers and Electronic Equipment. These are largely down to demand-pull dynamics as the AI thematic intensifies.

In Services, we see a much more subdued picture outside of industries with direct exposure to petroleum distillates: Air Transport, Truck Transport and Messengers and Couriers all reported double-digit year over year increases.

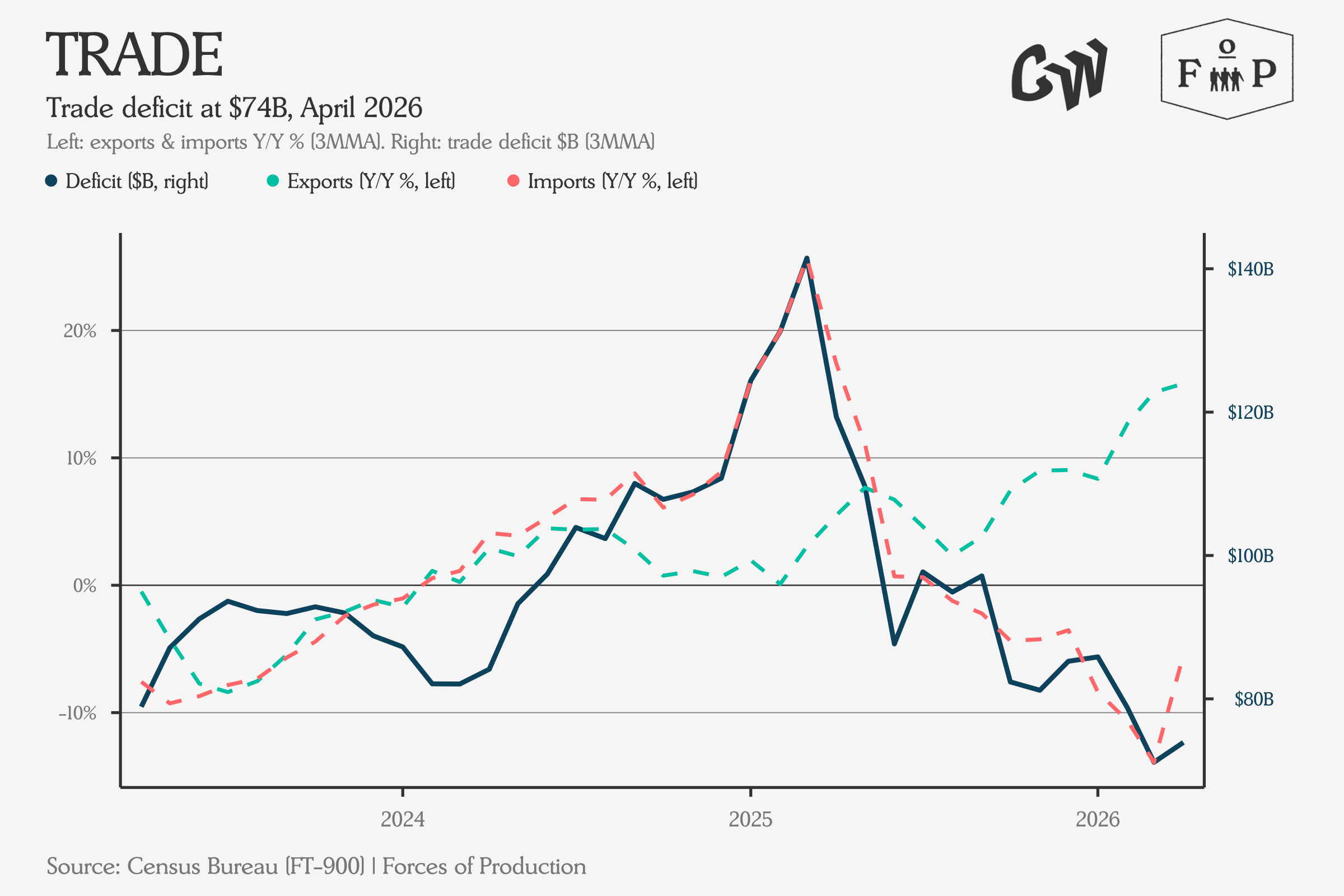

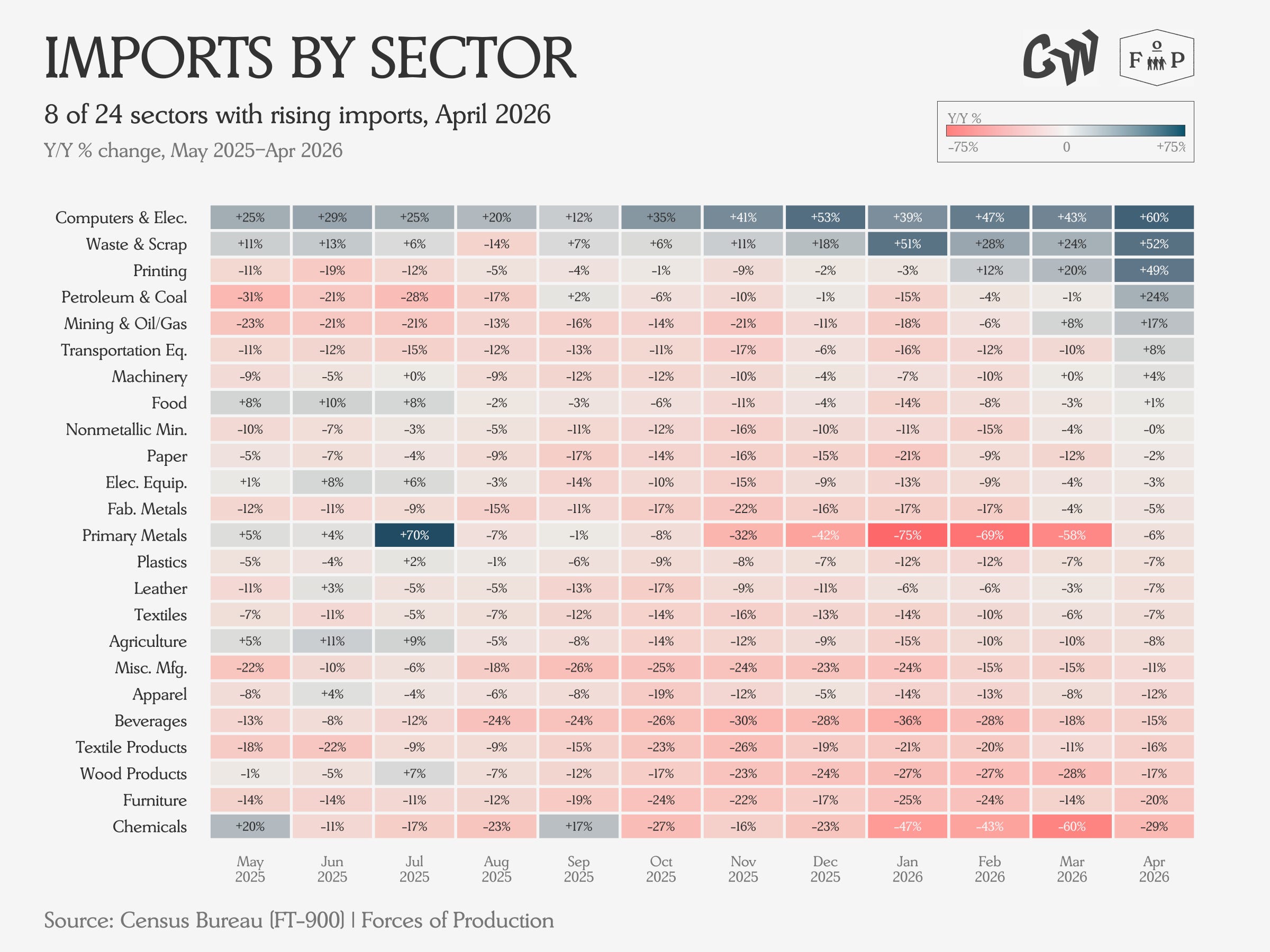

Trade

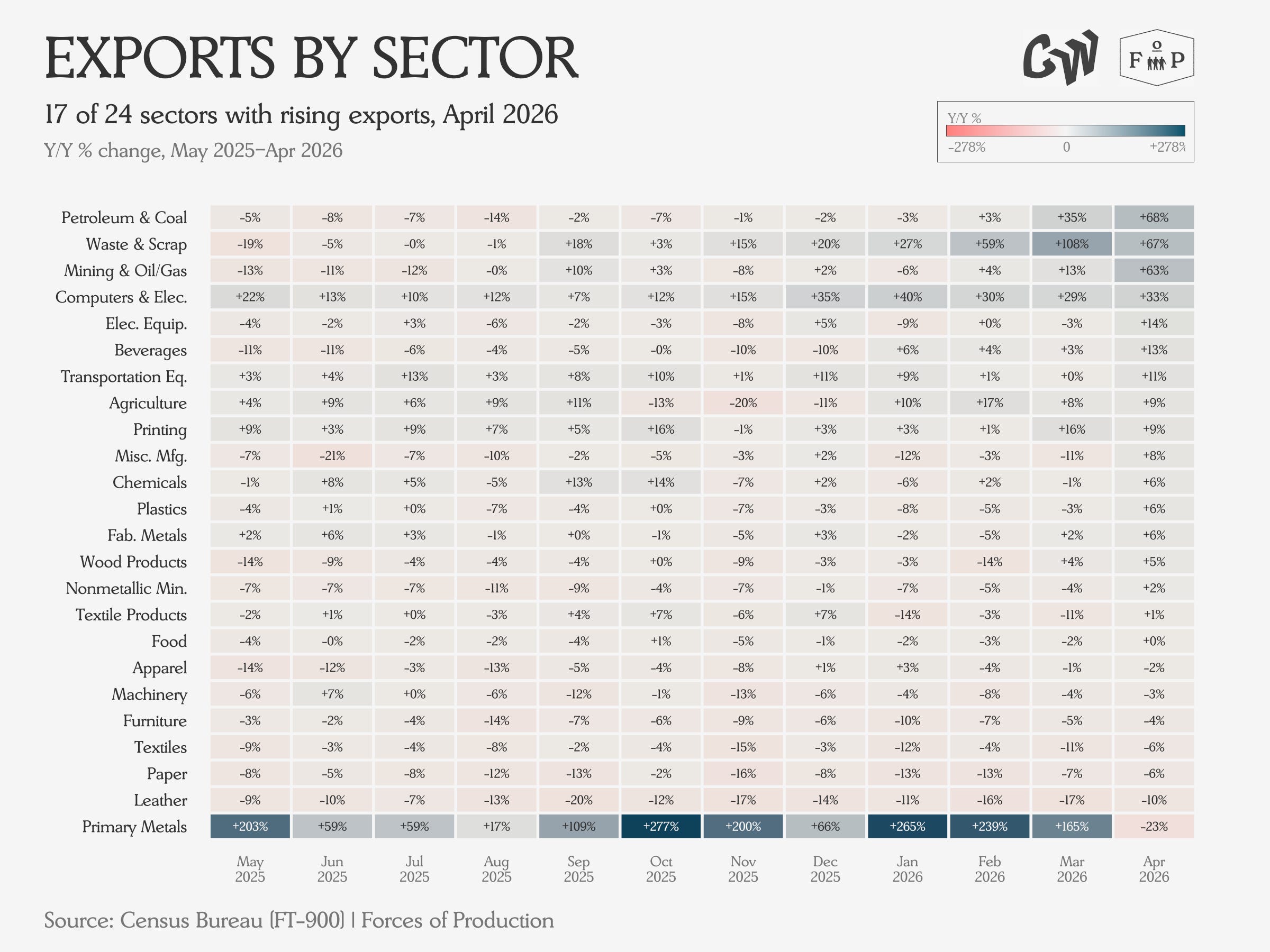

Exports continued to grow in the April data, supporting a narrowing of the trade deficit despite a slight bounceback in imports.

Going by sector, we see shrinking imports across much of the board, with the biggest declines for imported chemicals. As the Hormuz shock propagates, Chemicals are an important node to watch how it may force unexpected changes in trading patterns. Petroleum and Coal Products imports growth turned positive on the year in the April data, reflecting significant pricing impacts.

Exports grew in nearly two-thirds of sectors, year over year, in the April data, with price moves providing wind in the sails of the biggest gainers: the oil and gas complex and the computers and electrical equipment complex.